Navigating 2026 Federal Student Loan Repayment: A Comprehensive US Borrower’s Guide

Understanding the landscape of federal student loan repayment can often feel like navigating a complex maze. With continuous updates and new initiatives, staying informed is crucial for US borrowers. As we approach 2026, significant changes are on the horizon, particularly with the full implementation of the Saving on a Valuable Education (SAVE) Plan and other adjustments to existing income-driven repayment (IDR) options. This detailed guide aims to demystify these changes, providing you with the essential knowledge to make informed decisions about your student debt.

The federal government consistently reviews and revises its student aid policies to better support borrowers. These efforts are often driven by economic shifts, changes in educational costs, and the evolving needs of the workforce. The upcoming changes in 2026 are designed to offer more affordable and manageable repayment paths for millions of Americans. Whether you’re a recent graduate, a seasoned professional, or someone returning to education, comprehending these new federal student loan repayment plans is paramount to your financial well-being.

Our focus here will be on breaking down the specifics of the SAVE Plan, examining how it differs from previous IDR plans, and exploring its full benefits that will become active in July 2024 and fully implemented by 2026. We will also touch upon other relevant IDR plans, discuss eligibility requirements, and provide practical strategies for managing your student loans effectively. By the end of this article, you should have a clear roadmap for navigating your student loan repayment journey in 2026 and beyond.

The Evolution of Federal Student Loan Repayment Plans

Before diving into the specifics of the 2026 changes, it’s helpful to understand the historical context of federal student loan repayment. For decades, the primary repayment option was the Standard Repayment Plan, which typically involves fixed payments over 10 years. While straightforward, this plan often proved unaffordable for borrowers with lower incomes or higher debt loads.

In response to these challenges, income-driven repayment (IDR) plans were introduced. These plans tie monthly payments to a borrower’s income and family size, making them more affordable. Over the years, several IDR plans have emerged, each with its own set of rules and benefits:

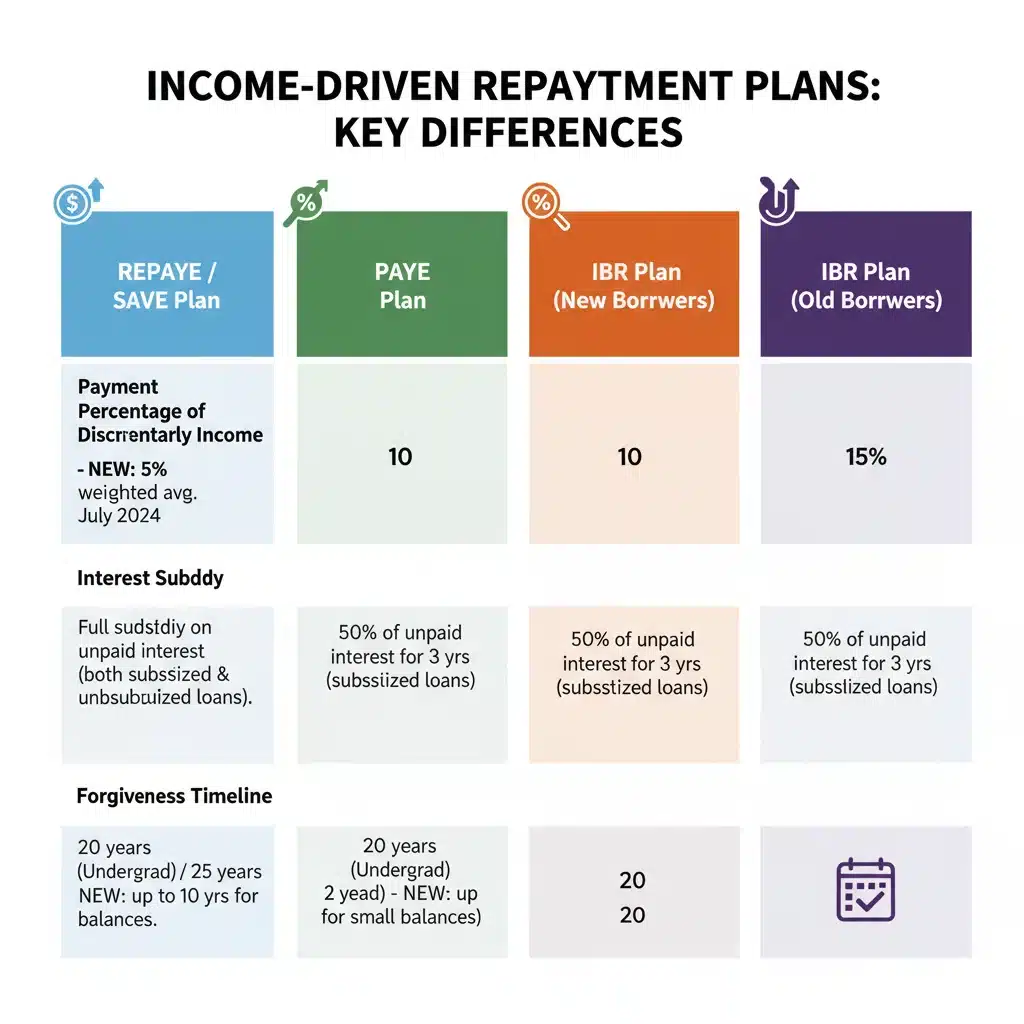

- Income-Based Repayment (IBR): Generally sets payments at 10% or 15% of discretionary income, with forgiveness after 20 or 25 years.

- Pay As You Earn (PAYE): Limits payments to 10% of discretionary income, with forgiveness after 20 years.

- Revised Pay As You Earn (REPAYE): Also sets payments at 10% of discretionary income, but applies to a broader range of loans than PAYE, with forgiveness after 20 or 25 years.

- Income-Contingent Repayment (ICR): Payments are calculated as either 20% of discretionary income or what you’d pay on a fixed 12-year plan, whichever is less, with forgiveness after 25 years.

These plans have provided crucial relief to many borrowers, but their complexity, varying eligibility rules, and sometimes insufficient interest subsidies have led to calls for further simplification and improvement. This brings us to the latest evolution: the SAVE Plan, which is set to significantly reshape student loan repayment in 2026.

Introducing the SAVE Plan: What Borrowers Need to Know for 2026

The Saving on a Valuable Education (SAVE) Plan is the most generous income-driven repayment plan to date, building upon and replacing the REPAYE Plan. While some benefits of the SAVE Plan went into effect in summer 2023, and more in July 2024, its full implementation with all its advantages will be firmly in place by 2026. For US borrowers, understanding the SAVE Plan’s features is critical for managing student loan repayment 2026.

Key Features of the SAVE Plan:

- Lower Monthly Payments: For undergraduate loans, payments are reduced from 10% to 5% of your discretionary income. For graduate loans, payments remain at 10%. If you have both undergraduate and graduate loans, your payment will be a weighted average between 5% and 10% based on the original principal balances of your loans.

- Higher Discretionary Income Threshold: The amount of income considered “discretionary” is significantly increased. Under SAVE, discretionary income is calculated as the difference between your adjusted gross income (AGI) and 225% of the federal poverty guideline for your family size (up from 150% in other IDR plans). This means a larger portion of your income is protected, resulting in lower monthly payments for most borrowers.

- Interest Subsidy: This is a game-changer. If your monthly SAVE Plan payment doesn’t cover the accrued interest, the government covers the remaining interest. This means your loan balance will not grow due to unpaid interest, even if your payment is $0. This prevents the common problem of “negative amortization,” where balances balloon despite making regular payments. This feature is particularly beneficial for those with low incomes and high loan balances.

- Shorter Path to Forgiveness for Smaller Balances: Borrowers with original principal balances of $12,000 or less will receive forgiveness after just 10 years of payments. For each additional $1,000 borrowed above $12,000, an additional year of payments is required, up to the maximum of 20 or 25 years. This accelerated forgiveness provides a faster pathway out of debt for many borrowers.

- Spousal Income Exclusion: If you are married and file separately, your spouse’s income will not be included in the calculation of your monthly payment under the SAVE Plan. This is a significant advantage for many married borrowers compared to other IDR plans where spousal income might be considered even if filing separately.

- Automatic Enrollment for Defaulted Borrowers: Borrowers who default on their federal student loans may be automatically enrolled in the SAVE Plan after successfully completing the Fresh Start initiative. This provides a clear and affordable path back to good standing.

The SAVE Plan is designed to be more accessible, more affordable, and more forgiving than previous IDR plans. Its full implementation by 2026 will mark a new era for federal student loan repayment, offering substantial relief to millions of US borrowers.

Who is Eligible for the SAVE Plan?

Most federal student loans are eligible for the SAVE Plan, including:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Direct PLUS Loans made to students

- Direct Consolidation Loans (that did not include Parent PLUS Loans)

Federal Family Education Loan (FFEL) Program loans and Perkins Loans are generally not directly eligible, but they can become eligible if you consolidate them into a Direct Consolidation Loan. However, if you consolidate Parent PLUS Loans, the resulting Direct Consolidation Loan is only eligible for the Income-Contingent Repayment (ICR) Plan, not SAVE. It’s crucial to understand your specific loan types when considering your options for student loan repayment 2026.

Comparing SAVE with Other Income-Driven Repayment Plans

To fully appreciate the benefits of the SAVE Plan, it’s helpful to see how it stacks up against other IDR options. While some older plans like PAYE and IBR will still exist for those already enrolled, SAVE is positioned to be the most attractive option for many new and existing borrowers.

Key Differences and Advantages of SAVE:

- Payment Calculation: As mentioned, SAVE uses 5% of discretionary income for undergraduate loans, significantly lower than the 10% or 15% of other plans. The expanded definition of discretionary income also means lower payments across the board.

- Interest Accrual: SAVE’s interest subsidy is a unique and powerful feature. Under other IDR plans, unpaid interest can capitalize (be added to your principal balance), causing your loan balance to grow even if you’re making payments. SAVE eliminates this issue, ensuring your balance won’t increase due to unpaid interest. This is a major advantage for student loan repayment 2026.

- Forgiveness Timeline: While most IDR plans offer forgiveness after 20 or 25 years, SAVE introduces an accelerated timeline for borrowers with smaller initial balances. This is a significant benefit for those who borrowed less.

- Spousal Income: The exclusion of spousal income for married borrowers filing separately under SAVE provides a distinct advantage over PAYE and IBR, which may still consider spousal income even with separate filing.

For many borrowers, especially those with undergraduate loans, lower incomes, or higher loan balances, the SAVE Plan will likely offer the lowest monthly payments and the most favorable terms for student loan repayment 2026. However, it’s always wise to use the Federal Student Aid Loan Simulator to compare all available options based on your specific financial situation.

Strategic Planning for Student Loan Repayment in 2026

With the full implementation of the SAVE Plan and other changes by 2026, proactive planning is essential. Here are some strategies for US borrowers to optimize their student loan repayment journey:

1. Understand Your Loan Types and Servicers:

Before making any decisions, know exactly what types of federal student loans you have (e.g., Direct Subsidized, Unsubsidized, PLUS, FFEL, Perkins) and who your loan servicer is. You can find this information by logging into your account on StudentAid.gov.

2. Utilize the Federal Student Aid Loan Simulator:

This powerful tool on StudentAid.gov allows you to input your specific loan details, income, and family size to see estimated monthly payments under all eligible repayment plans, including the SAVE Plan. It’s the best way to compare options and understand the real impact on your budget. This is indispensable for student loan repayment 2026 planning.

3. Consider Consolidation:

If you have FFEL Program loans or Perkins Loans, consolidating them into a Direct Consolidation Loan may make them eligible for the SAVE Plan. Be mindful that consolidating can sometimes lead to a longer repayment period and that consolidating Parent PLUS Loans has specific implications for IDR eligibility (only ICR is available). Weigh the pros and cons carefully.

4. Re-evaluate Your Income and Family Size Annually:

If you’re on an IDR plan, including SAVE, you’ll need to recertify your income and family size annually. Failing to do so can result in your payments reverting to the Standard Repayment Plan amount, and any unpaid interest may capitalize. Keep track of your recertification date and submit updated information promptly.

5. Explore Public Service Loan Forgiveness (PSLF):

If you work for a qualifying government or non-profit organization, the PSLF program can forgive the remaining balance on your Direct Loans after 120 qualifying monthly payments while on an IDR plan. Payments made under the SAVE Plan count towards PSLF. Ensure you understand PSLF requirements and submit an Employment Certification Form (ECF) annually.

6. Budget and Emergency Fund:

Even with lower payments, it’s crucial to budget effectively and build an emergency fund. Unexpected expenses can always arise, and having savings can prevent you from falling behind on payments. The reduced burden from student loan repayment 2026 under SAVE can free up funds for these vital financial goals.

7. Stay Informed About Future Changes:

Federal student loan policies can evolve. Regularly check official sources like StudentAid.gov and your loan servicer’s website for the latest updates and announcements. Subscribe to relevant newsletters or follow reputable financial news outlets. This ongoing vigilance is key to navigating student loan repayment 2026 and beyond successfully.

Potential Challenges and Considerations

While the SAVE Plan offers significant advantages, it’s important to be aware of potential challenges and nuances:

- Taxability of Forgiven Debt: Currently, under federal law, any loan balance forgiven under an IDR plan (including SAVE) may be considered taxable income by the IRS. This is a critical point to consider, especially for those anticipating a large forgiveness amount. However, legislation can change, and there have been temporary exemptions in the past. Consult a tax professional as you approach your forgiveness date.

- Administrative Complexity: Despite efforts to simplify, the federal student loan system can still be complex. Navigating applications, recertifications, and communication with servicers requires diligence. Keep detailed records of all correspondence and payments.

- Longer Repayment Period: While IDR plans offer lower monthly payments, they often extend the repayment period significantly (20-25 years, or even longer for some under SAVE). This means you’ll be in debt for a longer time, even if your monthly burden is lower.

- Impact on Credit: Consistently making on-time payments under any repayment plan, including SAVE, will positively impact your credit score. However, defaulting on loans will severely damage it.

Being prepared for these aspects is part of a comprehensive strategy for student loan repayment 2026.

Real-World Impact: Who Benefits Most from SAVE?

The SAVE Plan is particularly beneficial for several groups of US borrowers:

- Low-Income Borrowers: With the increased discretionary income threshold and the 5% payment rate for undergraduate loans, many low-income borrowers will see their monthly payments significantly reduced, potentially even to $0. The interest subsidy ensures their loan balances won’t grow.

- Borrowers with High Debt-to-Income Ratios: Individuals with large student loan balances relative to their income will find the SAVE Plan invaluable. The lower payments and interest subsidy prevent their debt from becoming an insurmountable burden.

- Recent Graduates: Young professionals often start their careers with lower salaries. The SAVE Plan provides an affordable entry into repayment, preventing early financial distress.

- Borrowers Pursuing Public Service: For those on the path to Public Service Loan Forgiveness (PSLF), the SAVE Plan offers the lowest payments while ensuring that their loan balance doesn’t grow, making their eventual forgiveness more impactful.

- Married Borrowers Filing Separately: The exclusion of spousal income under SAVE is a significant advantage for married individuals who choose to file their taxes separately, potentially leading to much lower payments.

These groups will experience the most profound positive effects on their student loan repayment 2026 plans.

The Future of Student Loan Repayment Beyond 2026

While the focus is currently on the full implementation of the SAVE Plan by 2026, it’s important to remember that federal student aid policies are dynamic. The Department of Education and Congress continuously evaluate the effectiveness of these programs and may introduce further changes in the future. Staying engaged with official announcements and understanding the broader economic context will help you adapt to any new developments.

The overarching goal of these reforms is to create a more equitable and sustainable student loan system. The SAVE Plan represents a significant step in that direction, aiming to reduce financial stress for millions of borrowers, prevent defaults, and ensure that higher education remains an accessible path to opportunity rather than a source of overwhelming debt.

Conclusion: Empowering US Borrowers for Student Loan Repayment 2026

The upcoming changes to federal student loan repayment plans, particularly the full rollout of the SAVE Plan by 2026, offer unprecedented relief and flexibility for US borrowers. With lower monthly payments, an innovative interest subsidy, and faster forgiveness timelines for smaller balances, the SAVE Plan is poised to transform how millions manage their student debt.

By understanding the nuances of the SAVE Plan, comparing it with other IDR options, and leveraging resources like the Federal Student Aid Loan Simulator, you can strategically plan your student loan repayment 2026. Proactive engagement, annual recertification, and staying informed about policy updates are key to optimizing your financial future.

Don’t let complex jargon deter you. Take the time to assess your situation, explore your options, and make choices that align with your financial goals. The tools and plans are in place to help you navigate your student debt successfully. Empower yourself with knowledge, and take control of your student loan repayment journey for 2026 and the years to come.