Mastering 2026 Tax Code Changes: Maximize Deductions & Avoid Penalties

The financial landscape is ever-evolving, and perhaps no area reflects this more keenly than tax law. As we draw closer to 2026, a significant array of potential 2026 Tax Code Changes looms on the horizon, promising to reshape individual and business finances across the nation. For many, the prospect of new regulations can be daunting, bringing with it concerns about increased complexity, potential liabilities, and the need for rigorous financial adjustments. However, with proactive planning and a clear understanding of the impending shifts, these changes can also present opportunities for savvy taxpayers to optimize their financial strategies, maximize deductions, and ensure compliance without unnecessary stress.

Understanding the nuances of the upcoming 2026 Tax Code Changes is not merely about avoiding penalties; it’s about strategic financial positioning. Whether you’re an individual taxpayer, a small business owner, or managing a large corporation, the implications of these changes will be far-reaching. From alterations in standard deductions and itemized deductions to modifications in business tax rates and investment income rules, every facet of your financial life could be touched. This comprehensive guide is designed to cut through the complexity, offering a clear roadmap to navigate the 2026 tax landscape. We will delve into five key strategies that will empower you to not only adapt but thrive amidst the new regulations, ensuring you are well-prepared to make the most of your financial future.

Our aim is to provide actionable insights and practical advice, transforming what might seem like a bureaucratic hurdle into a strategic advantage. By the end of this article, you will have a solid foundation for understanding the most critical aspects of the 2026 Tax Code Changes and be equipped with the knowledge to proactively implement strategies that safeguard and enhance your financial well-being. Let’s embark on this journey to demystify the tax code and turn potential challenges into tangible opportunities.

Understanding the Impending 2026 Tax Code Changes: What’s on the Horizon?

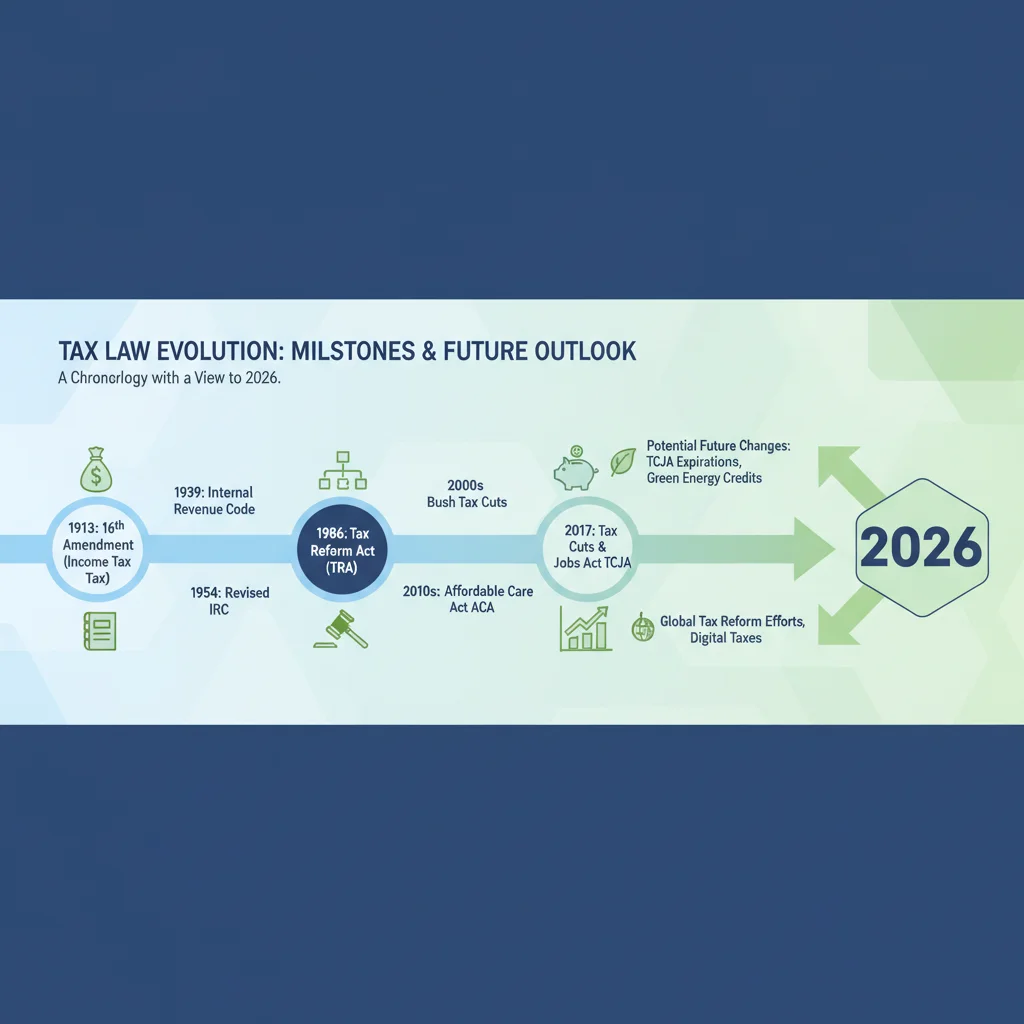

Before we dive into specific strategies, it’s crucial to grasp the foundational elements of the 2026 Tax Code Changes. While the exact details are still subject to legislative finalization, several key areas are anticipated to undergo significant transformation, primarily due to the expiration of certain provisions from the Tax Cuts and Jobs Act (TCJA) of 2017. This landmark legislation introduced a multitude of changes, many of which were temporary and are set to sunset at the end of 2025, thus ushering in a new era of tax regulations in 2026.

Individual Tax Provisions Set to Expire

One of the most impactful expirations concerns individual income tax rates. The TCJA reduced rates across nearly all income brackets, and without new legislation, these rates are expected to revert to their pre-TCJA levels. This could mean higher tax liabilities for many taxpayers, particularly those in higher income brackets. Additionally, the standard deduction, which was significantly increased by the TCJA, is also slated to decrease. This change will compel more taxpayers to evaluate whether itemizing deductions becomes more beneficial than taking the standard deduction, a decision that will require careful calculation and planning.

Furthermore, the personal exemption, which was eliminated under the TCJA, is likely to be reinstated. This could offer some relief to larger families, though its impact will vary depending on other deductions and credits available. The child tax credit, which saw a temporary expansion under the TCJA and later during the pandemic, is also a point of discussion. While its exact form in 2026 is uncertain, it’s an area where changes could significantly affect families with children.

Business Tax Implications

While many of the TCJA’s business tax provisions were made permanent, some aspects could still see adjustments. For instance, certain deductions related to business expenses, particularly those concerning research and development (R&D) and interest expenses, have undergone changes in their deductibility. Businesses need to stay abreast of these evolving rules to ensure they are maximizing their legitimate deductions.

The corporate tax rate, which was dramatically lowered from 35% to 21% by the TCJA, is generally considered permanent. However, discussions around potential adjustments to this rate, or the introduction of new corporate minimum taxes, are always part of the legislative discourse. Small businesses, in particular, need to monitor pass-through income deductions (Section 199A), which are also set to expire. The future of this deduction, crucial for many S corporations, partnerships, and sole proprietorships, will heavily influence their tax planning.

Estate and Gift Tax Considerations

The estate and gift tax exemption amounts were substantially increased by the TCJA. These higher exemption limits are also scheduled to sunset, meaning that without new legislation, the exemption amounts will revert to significantly lower levels, indexed for inflation. This change has profound implications for high-net-worth individuals and families engaged in estate planning, potentially bringing more estates into the taxable threshold. Proactive estate planning becomes even more critical in this context.

Other Notable Areas of Change

Beyond these major categories, other areas that might see modifications include capital gains taxes, net investment income tax (NIIT), and various tax credits related to education, energy efficiency, and retirement savings. The interplay of these changes can create a complex web of regulations that demands a holistic approach to tax planning. Keeping an eye on legislative developments and consulting with tax professionals will be paramount to navigating these shifts successfully.

The anticipation of the 2026 Tax Code Changes underscores the dynamic nature of tax law. Rather than viewing these as mere administrative hurdles, taxpayers should see them as a catalyst for strategic financial review and optimization. The following sections will outline five actionable strategies to help you effectively prepare for and adapt to this new tax environment, ensuring your financial well-being remains robust.

Strategy 1: Proactive Financial Review and Budget Adjustment

The first and arguably most crucial strategy in preparing for the 2026 Tax Code Changes is to conduct a thorough and proactive review of your current financial situation. This isn’t just about glancing at your bank statements; it’s about a deep dive into your income, expenses, investments, and overall financial goals. Understanding your current financial health provides the baseline necessary to anticipate the impact of new tax laws and make informed adjustments. This strategy is foundational, as it informs all subsequent tax planning efforts.

Assessing Your Current Income and Expenses

Begin by meticulously documenting all sources of income, including wages, business profits, investment returns, and any other revenue streams. Simultaneously, track your expenditures. Categorize expenses to identify areas where you might have flexibility or where changes in tax deductibility could have a significant impact. For individuals, this means understanding your take-home pay and discretionary spending. For businesses, it involves a detailed analysis of operational costs, revenue streams, and profit margins.

With potential increases in individual income tax rates and changes to standard deductions, your net income could be affected. By understanding your current income and expense patterns, you can project how these shifts might alter your disposable income or business profitability. This foresight allows you to identify potential shortfalls or surpluses and plan accordingly.

Revisiting Your Budget and Financial Goals

Once you have a clear picture of your current financial flows, it’s time to revisit your budget. The 2026 Tax Code Changes might necessitate adjustments to your spending habits or savings goals. For example, if your tax liability is projected to increase, you might need to allocate more funds towards tax savings or reduce discretionary spending. Conversely, if new deductions or credits become available that you qualify for, you might find yourself with more financial flexibility.

Consider how these changes might affect long-term financial goals such as retirement planning, college savings, or significant purchases. Adjusting your budget now, even before the changes take full effect, can prevent financial surprises down the line. This proactive approach ensures that your financial roadmap remains aligned with your objectives, even as the tax landscape shifts.

Leveraging Financial Planning Tools

Utilize financial planning software or consult with a financial advisor to help model different scenarios based on anticipated tax changes. These tools can project the impact of various income tax rates, deduction limits, and credit availability on your overall financial picture. By running these ‘what-if’ analyses, you can gain a clearer understanding of potential outcomes and develop robust contingency plans.

A comprehensive financial review and budget adjustment are not just about reacting to the 2026 Tax Code Changes; they are about taking control of your financial narrative. By understanding your current position and projecting future scenarios, you empower yourself to make strategic decisions that protect and grow your wealth, regardless of external economic or legislative shifts.

Strategy 2: Optimize Deductions and Credits Through Strategic Planning

With the impending 2026 Tax Code Changes, optimizing your deductions and credits will become more critical than ever. As some provisions expire and others are introduced or modified, a strategic approach to identifying and claiming all eligible tax benefits can significantly reduce your overall tax liability. This strategy requires a thorough understanding of both current and anticipated tax laws, coupled with meticulous record-keeping.

Re-evaluating Itemized vs. Standard Deduction

One of the most significant areas of impact for individual taxpayers will be the re-evaluation of the standard deduction versus itemized deductions. With the expiration of the TCJA’s increased standard deduction amounts, many taxpayers who previously opted for the standard deduction may find that itemizing becomes more advantageous in 2026. This necessitates a careful review of all potential itemized deductions, including:

- State and Local Taxes (SALT): While the $10,000 SALT cap imposed by the TCJA is a federal limitation, its future is a subject of ongoing debate. Understanding your state and local tax burden is crucial.

- Mortgage Interest: Deductions for home mortgage interest can be substantial for homeowners.

- Medical Expenses: The threshold for deducting medical expenses as a percentage of Adjusted Gross Income (AGI) can be a significant factor for those with high healthcare costs.

- Charitable Contributions: Keep detailed records of all charitable donations, as these can provide valuable deductions.

It’s important to keep meticulous records throughout the year for all potential itemized deductions. This foresight will allow you to make an informed decision when tax season arrives.

Maximizing Business Deductions for Small Businesses

For businesses, the 2026 Tax Code Changes bring particular attention to the Section 199A qualified business income (QBI) deduction, which is set to expire. If this deduction is not extended or replaced, many pass-through entities will see a significant increase in their taxable income. Businesses should:

- Monitor Legislative Developments: Stay informed about any potential extensions or new legislation regarding the QBI deduction.

- Review Expense Categorization: Ensure all legitimate business expenses are properly categorized and documented. This includes operating costs, depreciation, and employee benefits.

- Consider Entity Structure: Depending on the final tax code, some businesses might find it advantageous to re-evaluate their entity structure (e.g., S-corp, C-corp, LLC) to optimize tax treatment.

- R&D and Capital Expenditures: Understand the rules for deducting research and development costs and how capital expenditures are treated for depreciation purposes. These areas have seen recent changes and could be further impacted.

Leveraging Tax Credits

Tax credits offer a dollar-for-dollar reduction in your tax liability, making them incredibly valuable. While some credits may be modified, others may be introduced or expanded. Key areas to watch include:

- Child Tax Credit: As mentioned, this credit is a significant benefit for families. Understand the eligibility requirements and any potential changes to its value.

- Education Credits: Credits like the American Opportunity Tax Credit and Lifetime Learning Credit can offset college expenses.

- Energy Efficiency Credits: Credits for home energy improvements or electric vehicle purchases can provide substantial savings.

- Business Credits: Various business credits exist for things like hiring certain employees, investing in specific areas, or conducting R&D.

Optimizing deductions and credits is not a one-time task but an ongoing process. By staying informed about the 2026 Tax Code Changes and diligently tracking your financial activities, you can ensure you’re claiming every dollar you’re entitled to, thereby minimizing your tax burden and maximizing your financial resources.

Strategy 3: Strategic Investment and Retirement Planning Adjustments

The 2026 Tax Code Changes will undoubtedly extend their reach into investment and retirement planning, making it imperative for individuals to review and potentially adjust their long-term financial strategies. Changes in capital gains rates, dividend taxation, and retirement account rules can significantly impact the growth and accessibility of your nest egg. Proactive planning in this area is key to ensuring your investments remain tax-efficient and aligned with your retirement goals.

Revisiting Capital Gains and Investment Income

One of the most anticipated areas of change involves capital gains taxes. The current long-term capital gains tax rates (0%, 15%, and 20%) are tied to income thresholds that could shift with the expiration of individual income tax rate provisions. If these rates increase, or if certain income thresholds are lowered, the tax implications of selling appreciated assets could become more significant. Consider the following:

- Tax-Loss Harvesting: This strategy involves selling investments at a loss to offset capital gains and potentially a limited amount of ordinary income. With potential capital gains rate increases, the value of tax-loss harvesting could become even greater.

- Asset Location: Strategically placing different types of investments in various account types (e.g., tax-deferred, tax-exempt, taxable) can optimize their tax treatment. For instance, placing high-growth or high-dividend stocks in tax-advantaged accounts can defer or eliminate taxes on their earnings.

- Qualified Dividends: Understand how changes might affect the taxation of qualified dividends, which are currently taxed at long-term capital gains rates.

Consulting with a financial advisor specializing in investment tax planning can help you navigate these complexities and make informed decisions about your portfolio in light of the 2026 Tax Code Changes.

Optimizing Retirement Contributions and Withdrawals

Retirement accounts are powerful tools for tax-advantaged savings, and their optimal use can be influenced by tax code changes. Consider these aspects:

- Traditional vs. Roth Contributions: If individual income tax rates are expected to rise in 2026 and beyond, contributing to a Roth IRA or Roth 401(k) now might be more advantageous. This allows you to pay for current medical expenses out-of-pocket and allowing the HSA funds to grow tax-free for future healthcare costs in retirement. Conversely, if you expect to be in a lower tax bracket in retirement, traditional contributions might still be preferable.

- Required Minimum Distributions (RMDs): While the SECURE Act 2.0 pushed back the age for RMDs, any further changes to retirement account rules could impact your withdrawal strategies. Understand how these rules apply to your specific situation to avoid penalties.

- Mega Backdoor Roth and Backdoor Roth: For high-income earners, strategies like the mega backdoor Roth or backdoor Roth IRA might be affected by future legislative changes. Stay updated on these complex rules to ensure continued eligibility.

- Employer-Sponsored Plans: Maximize contributions to 401(k)s, 403(b)s, and other employer-sponsored plans, especially if your employer offers a matching contribution. This is essentially free money and a significant boost to your retirement savings, regardless of tax code changes.

Estate Planning Implications

As noted earlier, the estate and gift tax exemption amounts are set to decrease significantly. This makes strategic estate planning even more critical for high-net-worth individuals. Consider:

- Utilizing Current Exemption Amounts: If you anticipate being affected by lower exemption limits, consider making significant gifts now to utilize the higher current exemption amounts.

- Reviewing Trust Structures: Existing trusts might need to be reviewed and potentially modified to ensure they remain effective under the new tax regime.

- Business Succession Planning: For business owners, changes in estate tax laws can impact the transfer of business ownership. Develop a robust succession plan that accounts for these potential shifts.

Strategic investment and retirement planning adjustments in response to the 2026 Tax Code Changes are about protecting your future wealth. By being proactive and seeking expert advice, you can ensure your financial legacy is secure and optimized for the evolving tax environment.

Strategy 4: Leverage Tax-Advantaged Accounts and Vehicles

A cornerstone of effective tax planning, especially in anticipation of the 2026 Tax Code Changes, is the strategic utilization of tax-advantaged accounts and vehicles. These financial instruments are specifically designed to offer tax benefits, such as tax-deferred growth, tax-free withdrawals, or immediate tax deductions, which can significantly reduce your overall tax burden. Understanding and maximizing these tools can be a game-changer for both individuals and businesses.

Health Savings Accounts (HSAs)

HSAs are often lauded as having a ‘triple tax advantage,’ making them incredibly powerful. Contributions are tax-deductible, earnings grow tax-free, and qualified withdrawals for medical expenses are also tax-free. As healthcare costs continue to rise, and with potential shifts in tax rates, the value of an HSA becomes even more pronounced.

- Maximize Contributions: If you are eligible (enrolled in a high-deductible health plan), contribute the maximum allowed amount annually.

- Invest Funds: Unlike a typical savings account, many HSAs allow you to invest the funds, letting your money grow over time.

- Long-Term Strategy: Consider using your HSA as an additional retirement account by paying for current medical expenses out-of-pocket and allowing the HSA funds to grow tax-free for future healthcare costs in retirement.

529 Plans for Education Savings

For those saving for education, 529 plans offer significant tax advantages. While contributions are typically not federally tax-deductible, earnings grow tax-free, and qualified withdrawals for educational expenses are also tax-free. Many states also offer a state income tax deduction or credit for contributions.

- Early Contributions: The earlier you start contributing, the more time your investments have to grow tax-free.

- Gift Tax Exemption: Contributions to a 529 plan can qualify for the annual gift tax exclusion, allowing you to transfer wealth efficiently.

- Potential for Rollovers: Recent legislation has introduced the possibility of rolling over unused 529 funds to a Roth IRA, adding flexibility to these plans.

Charitable Giving Vehicles

With potential changes to itemized deductions and estate tax exemptions, strategic charitable giving vehicles become even more relevant. These can include:

- Donor-Advised Funds (DAFs): DAFs allow you to make an irrevocable charitable contribution, receive an immediate tax deduction, and then recommend grants to charities over time. This is excellent for bunching deductions.

- Qualified Charitable Distributions (QCDs): For individuals aged 70½ or older, QCDs from an IRA can satisfy RMDs and be excluded from taxable income, even if you don’t itemize.

- Charitable Remainder Trusts (CRTs): These trusts allow you to donate assets to charity while retaining an income stream for a specified period, offering tax benefits and fulfilling philanthropic goals.

Business-Specific Tax Vehicles

Businesses also have access to various tax-advantaged vehicles. While the 2026 Tax Code Changes might influence their specific rules, the principle of leveraging them remains constant:

- Qualified Retirement Plans (e.g., Solo 401(k), SEP IRA): Small business owners can contribute significantly more to these plans than to traditional IRAs, offering substantial tax deferral.

- Section 179 Expensing and Bonus Depreciation: These provisions allow businesses to deduct the full purchase price of qualifying equipment and software in the year they are put into service, rather than depreciating them over several years. Stay updated on the limits and eligibility for these deductions.

By actively incorporating these tax-advantaged accounts and vehicles into your financial strategy, you can effectively mitigate the impact of the 2026 Tax Code Changes, reduce your taxable income, and accelerate your wealth accumulation. It requires foresight and often the guidance of a tax professional to ensure you are utilizing them to their fullest potential and in compliance with all regulations.

Strategy 5: Seek Professional Guidance and Stay Informed

The fifth and perhaps most critical strategy for navigating the 2026 Tax Code Changes is to seek professional guidance and commit to staying informed. Tax law is inherently complex and constantly evolving. Attempting to decipher all the nuances and apply them correctly to your unique financial situation without expert help can lead to missed opportunities, costly errors, and unnecessary stress. A qualified tax professional or financial advisor can be an invaluable partner in this journey.

The Value of a Qualified Tax Professional

Engaging with a Certified Public Accountant (CPA), an Enrolled Agent (EA), or a tax attorney offers several distinct advantages:

- Expert Interpretation: Tax professionals have an in-depth understanding of current tax law and are continually updated on proposed and enacted changes. They can interpret the specific implications of the 2026 Tax Code Changes for your individual or business circumstances.

- Personalized Strategies: A good advisor doesn’t offer generic advice. They will analyze your entire financial picture – income, expenses, investments, family situation, business structure – to develop tailored strategies for maximizing deductions, optimizing investments, and minimizing liabilities.

- Proactive Planning: Rather than simply preparing your taxes at year-end, a professional can help you engage in proactive tax planning throughout the year, making adjustments as needed in response to legislative developments or changes in your financial situation.

- Compliance Assurance: They can ensure that all your tax filings are accurate and compliant with the latest regulations, reducing the risk of audits or penalties.

- Representation: In the event of an audit or inquiry from the IRS, a tax professional can represent you, providing peace of mind and expert advocacy.

Consider scheduling a consultation with a tax professional well in advance of 2026 to discuss your specific situation and develop a robust action plan.

Commitment to Staying Informed

While professional guidance is crucial, it’s also important for you, as a taxpayer, to remain engaged and informed. The legislative process can be dynamic, and proposals can change rapidly. Here’s how you can stay updated:

- Follow Reputable News Sources: Subscribe to financial news outlets, tax publications, and reputable blogs (like this one!) that cover tax policy and legislative developments.

- IRS Resources: The Internal Revenue Service (IRS) website is the official source for tax information, including updates on new laws, forms, and publications.

- Professional Communications: Your tax advisor should keep you informed of significant changes that impact your situation. Don’t hesitate to ask questions.

- Attend Webinars and Seminars: Many financial institutions and professional organizations offer webinars and seminars on upcoming tax changes. These can be excellent opportunities to learn and ask questions.

Remember, being informed doesn’t mean becoming a tax expert yourself, but it does mean understanding the general direction of tax policy and recognizing when it’s time to seek clarification from your professional advisor. This collaborative approach ensures that you are always one step ahead of the 2026 Tax Code Changes, allowing you to adapt swiftly and effectively.

Conclusion: Embracing the Future of Taxation

The impending 2026 Tax Code Changes represent more than just a series of legislative adjustments; they signify an opportunity for individuals and businesses to re-evaluate, optimize, and fortify their financial strategies. While the prospect of new tax laws can often evoke apprehension, approaching these changes with a proactive mindset and the right strategies can transform potential challenges into significant financial advantages. By understanding the core aspects of these changes and implementing the five key strategies discussed, you are not just reacting to the future; you are actively shaping your financial destiny.

From conducting a thorough financial review and adjusting your budget to strategically optimizing deductions and credits, leveraging tax-advantaged accounts, and, crucially, seeking professional guidance and staying informed – each strategy plays a vital role in building a resilient financial plan. The interconnectedness of these approaches means that a holistic strategy will yield the best results, ensuring that every aspect of your financial life is aligned with the evolving tax landscape.

The journey through the 2026 Tax Code Changes may require diligence and continuous learning, but with a clear understanding and well-executed plan, you can navigate these shifts with confidence. Embrace this period as a catalyst for financial growth and optimization. By taking action now, you empower yourself to not only minimize tax liabilities but also to maximize your wealth, secure your financial future, and achieve your long-term goals. The time to prepare is now, and with these strategies in hand, you are well-equipped to face the future of taxation head-on.