2026 Housing Market: Interest Rate Forecasts & Affordability Challenges

The 2026 Housing Market: A Deep Dive into Interest Rate Forecasts and Affordability Challenges

As we navigate the ever-evolving landscape of real estate, the focus inevitably shifts to future predictions. The 2026 housing market is already a hot topic among economists, potential homeowners, and investors alike. Will it be a year of recovery, continued challenges, or a surprising boom? Understanding the interplay of interest rates, inflation, supply and demand, and broader economic trends is crucial to deciphering what lies ahead. This comprehensive analysis will delve into the anticipated trajectory of the 2026 housing market, offering insights into interest rate forecasts, the persistent issue of affordability, and what these factors mean for various stakeholders.

Understanding the Current Housing Market Dynamics

Before we project into 2026, it’s essential to grasp the forces currently shaping the housing market. The post-pandemic era brought unprecedented volatility, characterized by surging demand, historically low interest rates, and a severe shortage of inventory. This combination led to rapid home price appreciation, pushing many prospective buyers out of the market. Subsequently, aggressive interest rate hikes by central banks aimed at curbing inflation have cooled demand significantly, leading to a recalibration of market expectations. However, inventory remains tight in many regions, preventing a drastic price collapse and instead fostering a market where prices are stabilizing or experiencing modest declines in some areas, while still appreciating in others.

The current environment is a delicate balance. High mortgage rates have reduced buyer purchasing power, but a persistent lack of new construction, coupled with homeowners reluctant to sell and lose their existing low-rate mortgages, keeps supply constrained. This ‘lock-in’ effect is a significant factor, preventing a flood of new listings that would typically accompany a cooling market. As a result, the market isn’t collapsing; rather, it’s adapting to a new normal of higher borrowing costs and tighter inventory.

Demographic shifts also play a vital role. The millennial generation, now in their prime home-buying years, continues to represent a substantial segment of potential buyers. Their purchasing power, however, is increasingly challenged by elevated prices and interest rates, forcing many to delay homeownership or seek more affordable alternatives in secondary markets. These underlying dynamics will inevitably carry forward and influence the 2026 housing market.

Interest Rate Forecasts for the 2026 Housing Market

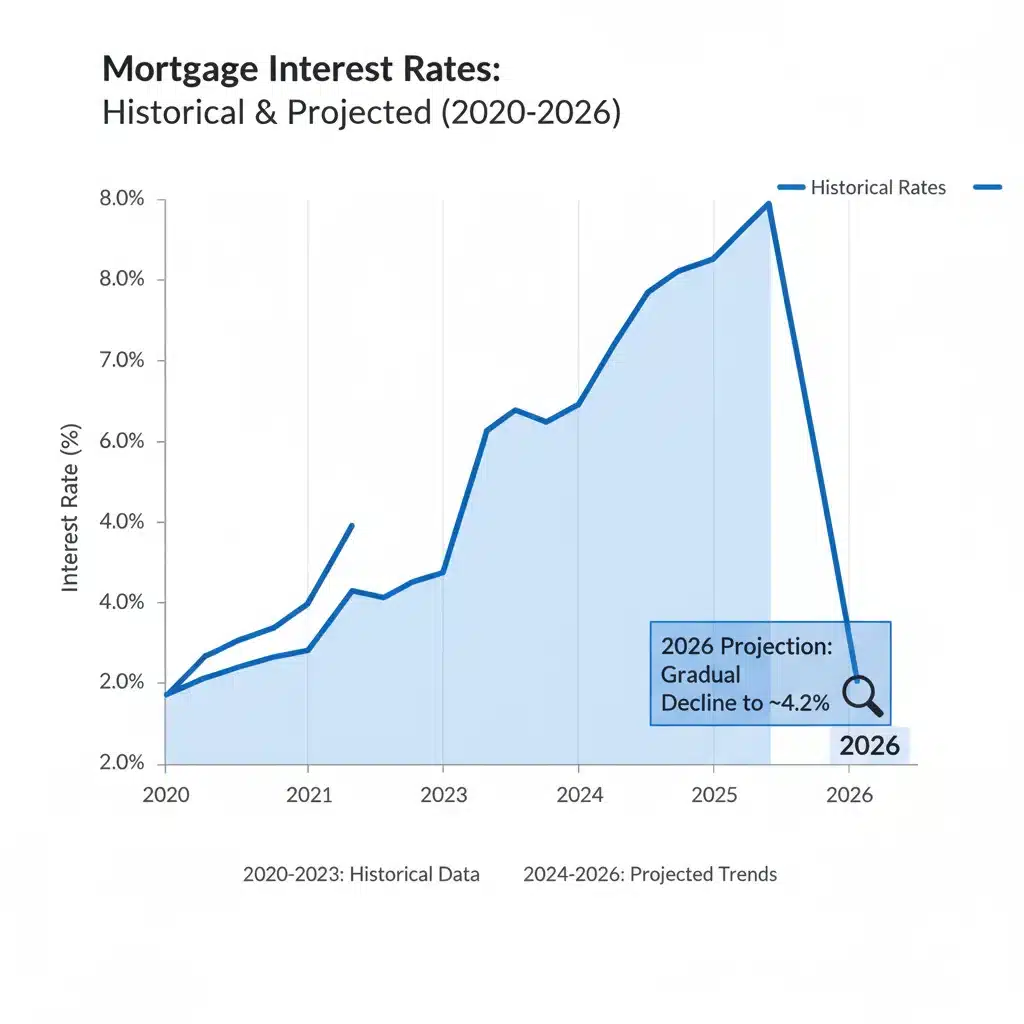

One of the most significant determinants of the 2026 housing market will undoubtedly be the trajectory of interest rates. Central banks, particularly the Federal Reserve in the U.S., have been on an aggressive campaign to combat inflation. While the peak of rate hikes may be behind us, the path to normalization is likely to be gradual and influenced by a multitude of economic indicators.

Factors Influencing Interest Rates

- Inflation: The primary driver of central bank policy. If inflation continues to moderate towards target levels (e.g., 2% in the U.S.), it could pave the way for rate cuts. Conversely, a resurgence in inflationary pressures could lead to rates remaining higher for longer.

- Economic Growth: A strong economy might allow central banks to keep rates elevated without stifling growth too much. A significant slowdown or recession, however, could prompt rate cuts to stimulate economic activity.

- Labor Market: A robust labor market, characterized by low unemployment and strong wage growth, can contribute to inflationary pressures and influence central bank decisions. A weakening labor market might signal a need for lower rates.

- Geopolitical Events: Global events, such as conflicts or supply chain disruptions, can have unforeseen impacts on energy prices, commodity costs, and overall economic stability, thereby affecting interest rate policy.

Expert Predictions for 2026

While no one has a crystal ball, a consensus among many economists suggests that interest rates, specifically mortgage rates, are likely to stabilize and potentially drift downwards from their recent highs by 2026. This isn’t to say we’ll return to the ultra-low rates of 2020-2021. Instead, the expectation is for rates to settle into a more historically normal range, perhaps between 5% and 6.5% for a 30-year fixed-rate mortgage, depending on the pace of inflation cooling and economic performance.

Some optimistic forecasts suggest that if inflation is decisively brought under control and a mild recession occurs, central banks might initiate more significant rate cuts, pushing mortgage rates closer to the 5% mark. However, other, more cautious predictions anticipate that persistent inflationary pressures or a resilient economy could keep rates in the higher end of that range, or even slightly above, for longer than many hope.

The key takeaway is that the era of exceptionally cheap money is likely over. The 2026 housing market will operate in an environment where borrowing costs are elevated compared to the recent past, but potentially more predictable and stable than the volatile period we’ve just experienced. This stability, even at a higher rate, can provide some certainty for buyers and sellers, allowing them to plan more effectively.

Affordability Challenges in the 2026 Housing Market

Even with potential stabilization or slight declines in interest rates, affordability is poised to remain a major hurdle in the 2026 housing market. The combination of elevated home prices, higher mortgage rates, and stagnant wage growth (relative to housing costs) has created a significant affordability crisis across many regions.

Key Contributors to Affordability Issues

- High Home Prices: Despite some cooling, home prices remain significantly higher than pre-pandemic levels. Years of underbuilding, especially of entry-level homes, have created a structural supply deficit that isn’t easily remedied.

- Elevated Mortgage Rates: Even if rates drop slightly, they will still be substantially higher than the 3% or 4% rates seen just a few years ago. This directly impacts monthly mortgage payments, requiring higher incomes to qualify for the same loan amount.

- Stagnant Wage Growth: While wages have seen some increases, they often haven’t kept pace with the dramatic rise in housing costs, widening the gap between what people earn and what they can afford to pay for housing.

- Inflationary Pressures on Other Goods: The cost of living has increased across the board, from groceries to energy, leaving less disposable income for housing down payments and monthly payments.

- Limited Inventory: The ‘lock-in’ effect, where existing homeowners are reluctant to sell their homes and lose their low mortgage rates, continues to constrain supply. This lack of inventory helps prop up prices, exacerbating affordability issues.

- Rising Property Taxes and Insurance: These ancillary costs associated with homeownership are also on the rise in many areas, adding to the overall financial burden.

Impact on Buyers and Sellers

For prospective first-time homebuyers, the 2026 housing market will likely continue to present significant challenges. Saving for a down payment is harder, and qualifying for a mortgage at higher rates requires a larger income. This may lead to continued reliance on family assistance, longer periods of renting, or a shift towards more affordable housing markets and smaller homes.

Existing homeowners looking to move up or downsize may also face a dilemma. While they might have substantial equity in their current homes, moving means giving up a potentially very low mortgage rate for a much higher one. This transaction cost, coupled with still-high purchase prices, could deter many from moving, further contributing to the inventory shortage.

The rental market will also feel the ripple effect. As homeownership becomes less accessible, demand for rentals increases, pushing up rental prices. This creates a vicious cycle where saving for a down payment becomes even harder for renters.

Regional Variations and Market Segmentation in 2026

It’s crucial to remember that the 2026 housing market will not be monolithic. Real estate is inherently local, and different regions, and even different segments within those regions, will experience varying dynamics.

Areas to Watch

- Sun Belt Markets: Regions that experienced massive population growth and price appreciation during the pandemic, such as parts of Florida, Texas, and Arizona, may see continued adjustments. While strong long-term demand remains, overvaluation in some areas combined with higher rates could lead to further price corrections or slower appreciation.

- Coastal Tech Hubs: Markets like San Francisco, Seattle, and New York, which are traditionally expensive, may continue to see price resilience due to high-paying jobs and limited supply, though affordability will remain extremely challenging.

- Midwest and Inland Markets: Many markets in the Midwest and other inland areas might offer relatively better affordability, attracting buyers priced out of coastal regions. These areas could see more stable growth, assuming local economic conditions remain strong.

- Rural vs. Urban: The shift towards remote work has blurred the lines between urban and rural living. While some urban centers are revitalizing, many suburban and exurban areas continue to attract buyers seeking more space and relative affordability.

Market Segments

- Luxury Market: Less sensitive to interest rate fluctuations, the luxury market often operates on different dynamics, driven by wealth preservation and investment.

- Entry-Level Homes: This segment will likely remain the most competitive due to high demand from first-time buyers and limited supply, exacerbating affordability issues.

- New Construction: Builders are adapting to market conditions, focusing on smaller, more affordable homes in some areas and offering incentives to buyers. New construction will be a key component in addressing the supply shortage, but rising material and labor costs remain a challenge.

The Role of Supply and Demand in the 2026 Housing Market

The fundamental laws of supply and demand will continue to exert immense influence on the 2026 housing market. The persistent undersupply of housing units, particularly affordable ones, is a structural issue that predates the pandemic and continues to fuel price appreciation even in the face of higher interest rates.

Supply-Side Factors

- Construction Pace: While homebuilding has picked up, it still lags behind historical averages and population growth in many areas. Labor shortages, supply chain issues, and rising material costs continue to hamper the pace of new construction.

- Existing Home Sales: The ‘lock-in’ effect, where homeowners with low mortgage rates are reluctant to sell, significantly reduces the supply of existing homes on the market. Until interest rates fall significantly or homeowners become more comfortable with higher rates, this trend is likely to persist.

- Zoning and Regulations: Restrictive zoning laws in many desirable areas limit density and new construction, contributing to the housing shortage. Reforms in these areas could unlock significant supply, but they are often politically challenging.

Demand-Side Factors

- Demographics: The large millennial generation, followed by Gen Z, continues to enter prime home-buying years, maintaining a baseline level of demand.

- Household Formation: Even with higher costs, new households are continuously forming, whether through marriage, young adults moving out, or immigration, all of which require housing.

- Investor Activity: While investor activity has cooled from its peak, institutional and individual investors continue to see real estate as a valuable asset class, particularly in the rental market, adding to demand.

The imbalance between supply and demand suggests that while price growth may moderate, significant price declines across the board are unlikely unless there’s a severe economic downturn or a dramatic increase in inventory. The 2026 housing market will likely see this tension continue, with limited supply providing a floor for prices in many areas.

Economic Outlook and its Impact on the 2026 Housing Market

The broader economic environment will serve as the backdrop for the 2026 housing market. A healthy economy, characterized by low unemployment and stable growth, generally supports a robust housing market, even with higher interest rates. Conversely, a recession or significant economic instability could introduce new challenges.

Potential Scenarios

- Soft Landing: This scenario involves inflation returning to target levels without a severe recession. In this case, interest rates might gradually decline, and the housing market could see stable prices with modest growth.

- Mild Recession: A shallow and short-lived recession could lead to more significant rate cuts from central banks, potentially stimulating housing demand. However, job losses and economic uncertainty could temper this effect, leading to some price softness.

- Stagflation: A less desirable scenario where high inflation persists alongside slow economic growth. This could keep interest rates elevated, further squeezing affordability and potentially leading to a prolonged period of housing market stagnation.

- Strong Economic Rebound: If the economy proves more resilient than expected, avoiding a recession and seeing sustained growth, interest rates might stay higher for longer. However, strong job growth and wage increases could help offset some affordability challenges.

The consensus leans towards a soft landing or a mild recession, suggesting that while challenges remain, the economic environment in 2026 might be more stable than the volatile period we have recently experienced. This stability, coupled with demographic tailwinds, could provide a foundation for a more predictable, albeit still competitive, 2026 housing market.

Strategies for Buyers, Sellers, and Investors in 2026

Navigating the 2026 housing market will require strategic planning for all participants.

For Prospective Buyers:

- Focus on Affordability: Prioritize homes within your budget, even if it means compromising on size or location. Explore first-time homebuyer programs and assistance.

- Strengthen Your Finances: Improve your credit score, save a substantial down payment, and get pre-approved for a mortgage to understand your borrowing power.

- Be Patient and Flexible: The market may still require patience. Be prepared to act quickly when the right opportunity arises, and consider expanding your search to include alternative neighborhoods or property types.

- Consider an Adjustable-Rate Mortgage (ARM): If you anticipate rates falling, an ARM could offer a lower initial rate, but understand the risks involved if rates rise. Many will still prefer the stability of a fixed-rate mortgage.

- Look Beyond the Hottest Markets: Explore emerging markets or slightly less competitive areas where your purchasing power might go further.

For Sellers:

- Price Realistically: The days of bidding wars on every property may be less common. Price your home competitively based on comparable sales and current market conditions.

- Enhance Your Property: Invest in curb appeal, essential repairs, and staging to make your home stand out in a market with more discerning buyers.

- Work with an Experienced Agent: A knowledgeable local real estate agent can provide invaluable insights into pricing, marketing, and navigating negotiations in a changing market.

- Understand Your Equity: If you have substantial equity, you’re in a stronger position. Factor in the cost of your next home and the potentially higher interest rate you’ll face.

For Investors:

- Focus on Cash Flow: In a higher interest rate environment, properties that generate strong rental income become even more attractive.

- Identify Growth Markets: Look for areas with strong job growth, population influx, and local government support for development.

- Consider Different Property Types: Beyond single-family homes, explore multi-family properties, short-term rentals (where regulations allow), or commercial real estate if it aligns with your strategy.

- Long-Term Perspective: Real estate is generally a long-term investment. Focus on fundamental value and be prepared to weather short-term fluctuations.

- Analyze Interest Rate Impact: Understand how different interest rate scenarios could affect your financing costs and potential returns.

Conclusion: Navigating the 2026 Housing Market

The 2026 housing market is shaping up to be a complex environment, influenced by a blend of moderating interest rates, persistent affordability challenges, and ongoing supply-demand imbalances. While a return to the frenzied pace of recent years is unlikely, a catastrophic crash also appears improbable for most regions. Instead, we are likely to see a market characterized by greater stability, but one that still demands strategic thinking and adaptability from all participants.

Interest rates are expected to stabilize and potentially see modest declines, offering some relief to buyers. However, the underlying issue of housing affordability, driven by stubbornly high home prices and increasing costs of living, will continue to be a dominant theme. Regional variations will be significant, with some markets experiencing more robust activity than others.

For buyers, patience, financial preparedness, and a willingness to explore different options will be key. Sellers will need to be realistic about pricing and presentation, while investors should prioritize cash flow and long-term value. Ultimately, those who understand the nuanced dynamics of the 2026 housing market and adapt their strategies accordingly will be best positioned for success.

Continuous monitoring of economic indicators, local market trends, and central bank policies will be essential to stay ahead in this evolving real estate landscape. The 2026 housing market may not be easy, but it will present opportunities for those who are well-informed and strategic.