2026 Social Security COLA: What Beneficiaries Should Anticipate

Understanding the 2026 Social Security Cost-of-Living Adjustment (COLA): What Beneficiaries Can Expect

For millions of Americans, Social Security benefits represent a vital source of income, providing financial stability during retirement, disability, or after the loss of a loved one. A crucial component of these benefits is the Cost-of-Living Adjustment, commonly known as COLA. This annual adjustment is designed to help Social Security beneficiaries maintain their purchasing power in the face of inflation. As we look ahead, understanding the 2026 COLA Forecast becomes increasingly important for current and future recipients. This comprehensive guide will delve into the intricacies of COLA, examine the factors that influence its calculation, and provide insights into what beneficiaries might anticipate for their 2026 Social Security payments.

What is the Social Security COLA and Why Does it Matter?

The Cost-of-Living Adjustment (COLA) is an annual increase in Social Security and Supplemental Security Income (SSI) benefits. Its primary purpose is to counteract the effects of inflation, ensuring that the value of these benefits does not erode over time. Without COLA, the fixed income of beneficiaries would gradually lose its purchasing power as the cost of goods and services rises. This adjustment is mandated by law and is a critical mechanism for protecting the financial well-being of millions of Americans who rely on Social Security.

The significance of COLA cannot be overstated. For many retirees, Social Security constitutes a substantial portion, if not all, of their monthly income. A robust COLA can mean the difference between financial stability and struggling to meet basic needs, especially during periods of high inflation. Conversely, a low or non-existent COLA can put significant strain on household budgets. Therefore, accurately predicting and understanding the 2026 COLA Forecast is paramount for effective financial planning.

How is the COLA Calculated? The CPI-W Connection

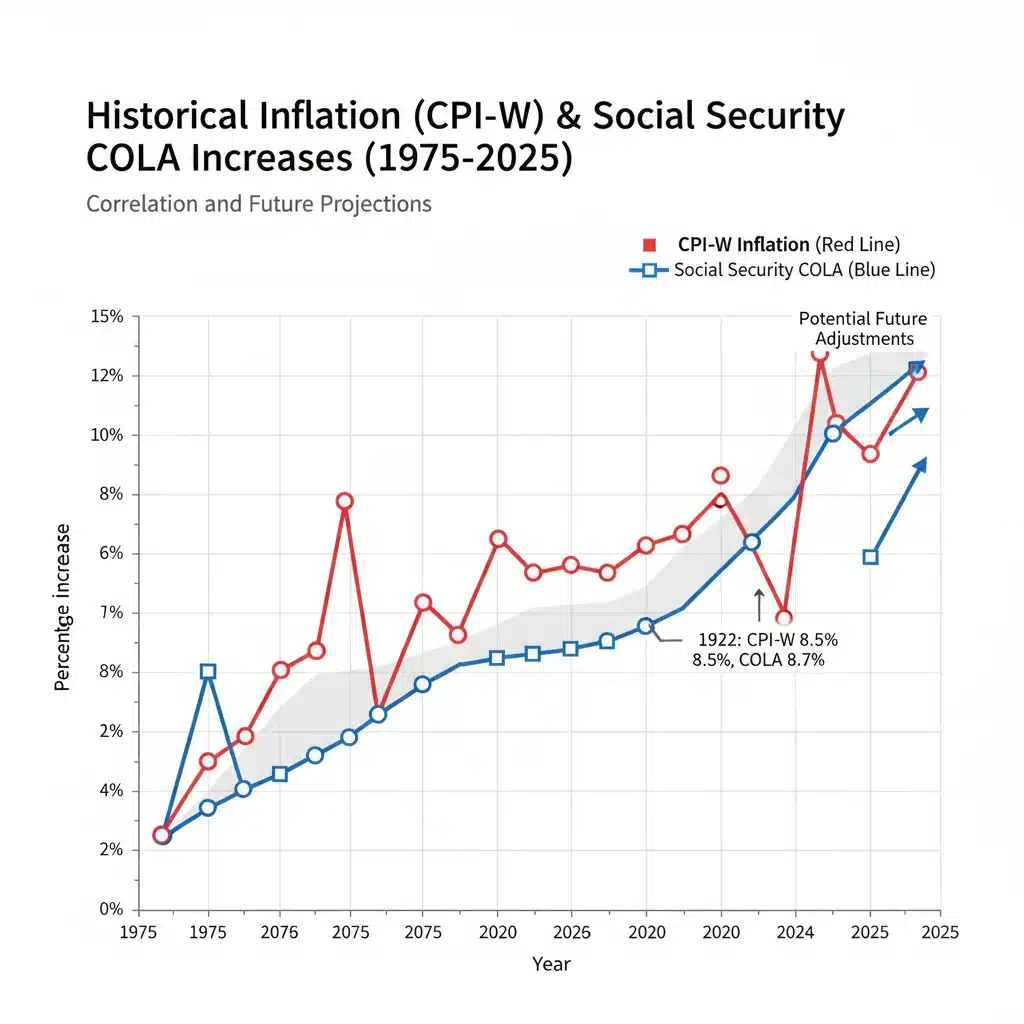

The Social Security Administration (SSA) determines the annual COLA based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This specific index measures the average change over time in the prices paid by urban wage earners and clerical workers for a market basket of consumer goods and services. The calculation method is as follows:

- The CPI-W for the third quarter (July, August, and September) of the current year is compared to the CPI-W for the third quarter of the previous year in which a COLA was effective.

- If there is an increase, the percentage increase is rounded to the nearest one-tenth of one percent.

- This percentage increase becomes the COLA for the following year. If there is no increase, or if the CPI-W declines, there is no COLA for that year.

It’s important to note that the COLA is typically announced in October of each year and takes effect in December, with the increased benefits appearing in January payments. For the 2026 COLA Forecast, the SSA will be looking at CPI-W data from the third quarter of 2025 compared to the third quarter of 2024 (or the last year a COLA was effective). Understanding this methodology is key to grasping the potential outcomes for your future benefits.

Key Economic Indicators Influencing the 2026 COLA Forecast

Forecasting the 2026 COLA Forecast requires a careful examination of various economic indicators, primarily those that impact inflation. The CPI-W, while specific, is influenced by broader economic trends. Here are the main factors to watch:

- Inflation Rates: The most direct driver of COLA. Sustained high inflation will likely lead to a higher COLA, while low inflation could result in a minimal or no adjustment. We need to monitor general consumer price trends, particularly in areas like energy, food, and housing, which significantly impact the CPI-W.

- Energy Prices: Fluctuations in oil and gas prices have a substantial effect on transportation costs and, consequently, the overall cost of living. A surge in energy prices can quickly push inflation upwards.

- Food Prices: Essential goods like food are a significant component of household budgets. Increases in food prices due to supply chain issues, weather events, or other factors directly contribute to higher CPI-W readings.

- Housing Costs: Rent and homeownership costs, including utilities, are a major expenditure for many. Rising housing costs can exert upward pressure on the CPI-W.

- Wage Growth: While not directly used in the COLA formula, strong wage growth can contribute to inflationary pressures as consumers have more disposable income, leading to increased demand for goods and services.

- Global Economic Conditions: International events, such as geopolitical conflicts, trade policies, and global supply chain disruptions, can have a ripple effect on domestic inflation rates and, by extension, the COLA.

- Federal Reserve Policy: The Federal Reserve’s monetary policy, particularly interest rate decisions, aims to manage inflation. Higher interest rates can cool down the economy and curb inflation, potentially leading to lower COLA adjustments.

Analysts and economists closely track these indicators throughout the year to project the likely COLA. For the 2026 COLA Forecast, we will need to observe how these elements evolve through 2024 and 2025.

Historical COLA Trends: A Look Back to Inform the Future

Examining past COLA adjustments can offer valuable context for understanding potential future trends. Historically, COLA percentages have varied significantly, reflecting different economic periods:

- High Inflation Eras: During periods of high inflation, such as the late 1970s and early 1980s, COLA adjustments were substantial, often reaching double digits. This was a direct response to rapidly rising living costs.

- Periods of Low Inflation: In contrast, years with low inflation have seen minimal COLA increases, and in some years, there was no COLA at all (e.g., 2010, 2011, 2016). These periods highlight the direct link between inflation and the adjustment.

- Recent Volatility: The 2020s have seen more volatile COLA adjustments, with a significant increase in 2022 and 2023 due to post-pandemic inflationary pressures, followed by a more moderate adjustment in 2024. This recent volatility underscores the unpredictable nature of economic forces.

Understanding these historical patterns helps set expectations. While no two economic cycles are identical, the past demonstrates the strong correlation between inflation and COLA. When considering the 2026 COLA Forecast, it’s prudent to account for the possibility of continued economic fluctuations.

Early Projections and Expert Opinions for the 2026 COLA Forecast

While it is still early, various organizations and economists begin to release preliminary projections for the 2026 COLA Forecast well in advance. These early estimates are often based on current economic trends, future inflation expectations, and historical data. It’s crucial to remember that these are forecasts and subject to change as new economic data becomes available.

Factors Potentially Leading to a Higher 2026 COLA:

- Persistent Inflationary Pressures: If global supply chain issues persist, energy prices remain elevated, or housing costs continue to climb through 2024 and 2025, it could lead to a higher COLA.

- Strong Consumer Demand: Robust consumer spending, fueled by a healthy job market, can keep demand high and contribute to rising prices for goods and services.

- Geopolitical Instability: Unforeseen global events can disrupt markets and supply chains, causing sudden spikes in commodity prices that impact inflation.

Factors Potentially Leading to a Lower 2026 COLA:

- Economic Slowdown or Recession: A significant economic downturn would likely reduce consumer demand, potentially leading to lower inflation or even deflation, thus decreasing the COLA.

- Successful Inflation Control by the Federal Reserve: If the Federal Reserve’s policies effectively bring inflation back to its target levels, the COLA will naturally be lower.

- Stabilization of Supply Chains: Improvements in global supply chains could lead to lower production costs and, consequently, lower consumer prices.

As 2024 progresses and into 2025, more concrete data will emerge, allowing for more precise predictions regarding the 2026 COLA Forecast. Beneficiaries should monitor reputable financial news sources and the Social Security Administration’s official announcements for the most up-to-date information.

Impact of the 2026 COLA on Beneficiaries

The 2026 COLA Forecast will have a direct and tangible impact on the monthly benefits received by millions of Americans. Here’s a breakdown of what beneficiaries should consider:

Increased Purchasing Power (with a positive COLA):

If the COLA is positive, beneficiaries will see an increase in their monthly payments. This is designed to help them afford the same level of goods and services as before, despite rising prices. For individuals on fixed incomes, even a small percentage increase can make a significant difference in their ability to cover daily expenses.

Medicare Premiums:

It’s crucial to remember the interplay between COLA and Medicare Part B premiums. While the COLA increases benefits, Medicare Part B premiums are often deducted directly from Social Security checks. In some years, a significant portion of the COLA increase can be absorbed by rising Medicare costs. The ‘hold harmless’ provision protects many beneficiaries from having their net Social Security benefit decrease due to Medicare premium increases, but this provision has specific rules and doesn’t apply to everyone (e.g., new enrollees, modified adjusted gross income over certain thresholds).

Taxation of Benefits:

An increase in Social Security benefits due to COLA could potentially push some beneficiaries into a higher income bracket, leading to a larger portion of their Social Security benefits being subject to federal income tax. The thresholds for taxing Social Security benefits are not adjusted for inflation, meaning that as benefits increase, more people may find themselves paying taxes on them. This is an important consideration when assessing the net impact of the 2026 COLA Forecast.

Financial Planning and Budgeting:

Regardless of the COLA percentage, beneficiaries should incorporate this adjustment into their annual financial planning. Understanding the estimated increase (or lack thereof) allows for more accurate budgeting and helps individuals determine if they need to adjust their spending habits or explore other income sources.

Preparing for the 2026 COLA: Tips for Beneficiaries

Proactive planning is essential for maximizing the benefits of COLA and mitigating any potential financial challenges. Here are some tips for beneficiaries as they anticipate the 2026 COLA Forecast:

- Stay Informed: Regularly check official sources like the Social Security Administration (SSA) website and reputable financial news outlets for updates on inflation data and COLA projections. The official announcement typically comes in October.

- Review Your Budget Annually: Even without a COLA, it’s good practice to review your monthly budget to account for changes in expenses. Once the 2026 COLA is announced, adjust your budget to reflect the new benefit amount and any changes in Medicare premiums.

- Understand Medicare Part B Premiums: Be aware of how Medicare Part B premiums are set and how they interact with your Social Security benefits. If you are not covered by the ‘hold harmless’ provision, a higher COLA might lead to a larger deduction for Medicare.

- Consider Tax Implications: If your income is close to the thresholds for Social Security benefit taxation, a COLA increase could impact your tax liability. Consult with a tax professional to understand potential implications and strategies.

- Explore Other Income Streams: If the COLA is lower than expected or if you find your expenses are consistently outpacing your benefits, consider exploring additional income sources, such as part-time work, investments, or other retirement savings.

- Monitor Your Spending: Keep a close eye on your spending habits. Identifying areas where you can cut back can provide a financial cushion, especially if the COLA does not fully keep pace with your personal cost of living.

- Consult a Financial Advisor: A financial advisor can help you integrate your Social Security benefits, including COLA adjustments, into your broader retirement plan, ensuring long-term financial security.

The Broader Discussion: COLA Adequacy and Future Reforms

Beyond the immediate 2026 COLA Forecast, there’s an ongoing discussion about whether the current COLA calculation method adequately reflects the actual cost of living for seniors. Critics often argue that the CPI-W, which focuses on urban wage earners and clerical workers, does not accurately capture the spending patterns of retirees, who typically spend more on healthcare and housing than the general working population.

Alternative indices, such as the Consumer Price Index for the Elderly (CPI-E), have been proposed as a more appropriate measure. The CPI-E theoretically would place a greater weight on healthcare costs, which tend to rise faster than other goods and services. If the COLA were calculated using the CPI-E, it could potentially result in higher annual adjustments for beneficiaries.

However, switching to a different index would involve complex political and economic considerations, including the potential impact on the solvency of the Social Security trust funds. This debate highlights the challenges in ensuring that Social Security benefits remain robust and equitable for all beneficiaries.

Frequently Asked Questions about COLA

When is the 2026 COLA announced?

The official 2026 COLA will be announced by the Social Security Administration in October 2025, based on inflation data from the third quarter of 2025.

Will my Social Security benefits always increase with COLA?

Your benefits will increase if there is a positive COLA. If the CPI-W does not show an increase, then there will be no COLA for that year, and your benefits will remain the same.

Does COLA apply to all Social Security benefits?

Yes, COLA applies to all Social Security benefits, including retirement, disability, and survivor benefits, as well as Supplemental Security Income (SSI).

How does COLA affect Medicare Part B premiums?

Medicare Part B premiums are often deducted from Social Security benefits. While COLA increases your benefits, rising Medicare premiums can offset some or all of that increase, especially if you are not protected by the ‘hold harmless’ provision.

Can the COLA be negative?

No, the COLA cannot be negative. If the CPI-W decreases, the COLA will be zero, meaning benefits will not decrease. They will remain at the same level as the previous year.

Where can I find the most accurate COLA information?

The most accurate and official information regarding the COLA will always come directly from the Social Security Administration (SSA) website (www.ssa.gov).

Conclusion: Staying Ahead of Your Social Security Benefits

The 2026 COLA Forecast is a critical piece of information for current and future Social Security beneficiaries. While it’s too early for definitive numbers, understanding the underlying mechanisms, economic indicators, and historical trends provides a solid foundation for anticipation and planning. The COLA’s role in preserving the purchasing power of benefits is indispensable, ensuring that millions of Americans can navigate the economic landscape with greater confidence.

By staying informed about inflation trends, monitoring expert projections, and proactively managing your personal finances, you can better prepare for the eventual COLA announcement. Remember that Social Security is a dynamic system, and being knowledgeable about its adjustments is key to securing your financial well-being in the years to come. Continue to check official SSA sources and financial news as 2024 and 2025 unfold to get the most accurate picture of what the 2026 COLA Forecast will bring.